New SSS Contribution Table 2025

Confused about how to compute and pay your SSS contributions properly?

Wondering why—in this digital age—the entire process of remitting contributions can’t be fully online? Frustrated with the late posting of your payments when it’s supposed to be instant?

Those are the birth pains of implementing the new Social Security Law and an SSS program for the real-time posting of contributions.

While adjusting to big changes is difficult, you can arm yourself with knowledge so you won’t waste time and effort dealing with your SSS contributions.

Here’s everything you need to know about computing your SSS contribution using the latest SSS contribution tables.

Related: SSS Online Registration Guide: 4 Easy Steps

Table of Contents

Who Can Pay SSS Contribution?

All employees, self-employed individuals, non-working spouse, and OFWs up to age 60 with an existing SSS number can pay their SSS contribution to begin or continue their coverage.

Covered members are entitled to social security benefits upon illness, unemployment, childbirth/miscarriage, disability, retirement, or death.

Related: How to Apply for SSS Unemployment Benefit: An Ultimate Guide

Unemployed Filipinos can only pay contributions as voluntary members if they’re previously covered as employed, self-employed, or OFW members with at least one month of posted contribution.

The SSS doesn’t allow contributing for the first time as a voluntary member without being registered as an employed, self-employed, or OFW member. Voluntary members can only contribute to continue their SSS coverage after they get separated from employment.

Self-employed members of the informal economy, such as farmers and fishermen, can also voluntarily pay their SSS contribution. Since they are the most vulnerable member category, the SSS has offered them a more flexible contribution schedule that allows them to pay their monthly contribution anytime within the last twelve months before their payment schedule. Under the new program, if their payment due is on October 2022, they can pay from October 2021 to September 2022. Giving them a longer grace period for making payments than the revised three-month period before their scheduled payments1.

Why Pay Your Contribution Regularly?

Especially if you’re on a limited budget, your monthly SSS contribution seems like an added expense. However, you’ll realize its value when you’re sick, injured, laid off, short of cash, or retiring.

Paying SSS contributions forces you to save for the future. While you’re still earning income, it’s good to consistently build your financial safety net for retirement by paying SSS contributions.

Also, the SSS uses the total number and amount of paid contributions as the basis for granting and computing a member’s benefit.

To qualify for an SSS benefit or loan, members must meet these requirements:

- Salary loan – At least six posted monthly contributions for the last 12 months with at least 36 posted monthly contributions.

- Sickness/Maternity benefit – At least three posted monthly contributions within 12 months before the semester of sickness, injury, childbirth, or miscarriage.

- Disability benefit – At least one month of posted contribution before the semester of disability.

- Retirement benefit – At least 120 posted monthly contributions before the semester of retirement to receive a monthly pension.

- Death benefit – At least 36 posted monthly contributions before the semester of the member’s death for the beneficiaries to receive a monthly pension.

- Funeral Benefit – at least one contribution posted before the member’s death.

- Unemployment/Involuntary separation benefit – At least 36 posted monthly contributions, 12 months of which should be within the 18 months before the month the member loses his/her job.

How To Compute Your Monthly SSS Contribution: The Basics

The amount that members remit to the SSS depends on two factors:

- Membership type – Employed, kasambahay, self-employed, voluntary, non-working spouse, and OFW members have different contribution amounts. Contributions of employees, kasambahays, and certain OFWs are deducted from their monthly salary and remitted to the SSS (along with the employer’s share of contribution) by their respective employers. Others have to pay their entire contribution.

- Monthly salary credit (MSC) – The Social Security Law defines the MSC as “the compensation base for contributions and benefits.” The SSS uses the MSC to compute the required contribution for members based on their monthly income. The higher your monthly earnings, the higher your MSC is. The higher your MSC, the higher your contribution becomes. On the SSS contribution table, you’ll find the MSC corresponding to your income range.

The New SSS Contribution Schedule

Before you begin computing your contribution, understand the key changes to the SSS Contribution Schedule following the implementation of the Social Security Act of 2018.

Beginning January 2023, the contribution rate has increased to 14%2 of the MSC and will continue to rise by 1% every other year until it reaches 15% by 2025.

The new law has also increased the minimum MSC from ₱3,000 in 2021 to ₱4,000 in 2023. This change will affect SSS members except for Kasambahay and Overseas Filipino Workers, whose minimum MSC will remain at ₱1,000 and ₱8,000, respectively.

Likewise, the maximum MSC will increase from ₱25,000 in 2021 to ₱30,000 in 2023.

What do these changes mean? You’re paying a higher monthly contribution now. But this will also increase your SSS benefits since they’re computed based on a higher MSC.

Ultimately, the SSS contribution hike will extend the SSS fund life, which raises your chance of receiving retirement benefits in the future.

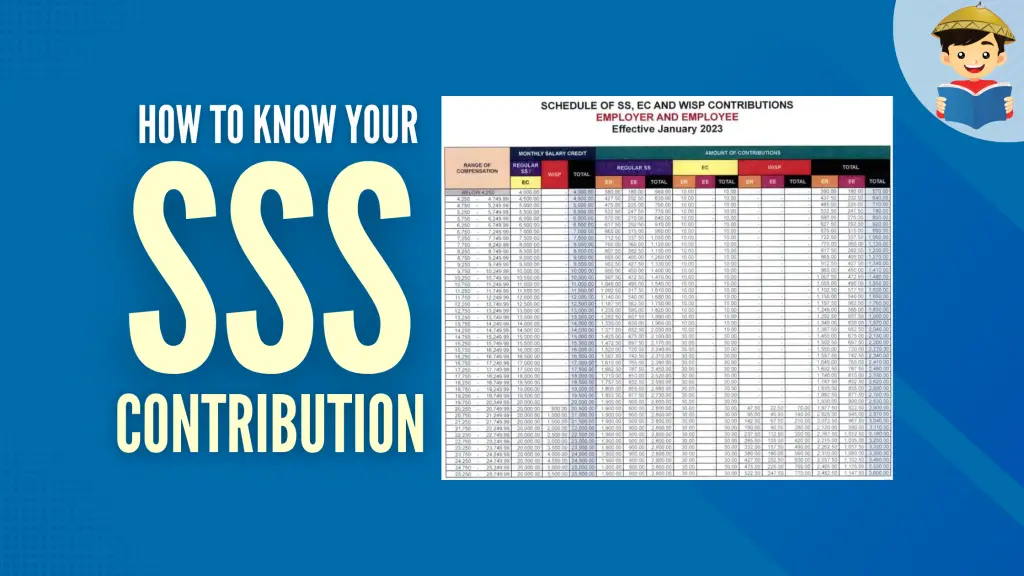

The 2023 SSS Contribution Table

1. Employed Members

Of the 14% contribution rate, the employee pays 4.5% through monthly salary deductions, while the employer shoulders the remaining 9.5%3.

Additionally, employers pay the monthly contribution for the Employees’ Compensation (EC) Program, which is ₱10 per employee earning below ₱15,000 or ₱30 per employee earning ₱15,000 and above.

Employers are required to remit all those contributions to the SSS on time.

For employers and employees, here’s how to determine the monthly contribution using the new SSS contribution table:

1. On the leftmost column (“Range of Compensation”), find the salary bracket where the current monthly income falls and its corresponding Monthly Salary Credit (MSC) on the “Total” column.

Only focus on the MSC for now. We’ll discuss what Mandatory Provident Fund or WISP means later on.

For example, this new table shows employees earning between ₱19,750 and ₱20,249.99 have an MSC of ₱20,000.

2a. If you’re an employer: Find your share of contribution for a particular employee on the ER column corresponding to the employee’s MSC. Per employee with an MSC of ₱20,000, you must pay ₱1,900 for the SSS contribution plus ₱30 for the EC contribution. The total amount to pay out of pocket is ₱1,930.

2b. If you’re an employee: Find your monthly deduction for SSS contribution on the EE column corresponding to your MSC. Using the same example, if your MSC is ₱20,000, your employer should deduct ₱900 from your monthly salary.

3. Look for the amount in the rightmost column to know the total monthly contribution. For an employee with an MSC of ₱20,000, the total monthly contribution is ₱2,830 (₱900 employee’s share + ₱1,900 employer’s share with EC contribution). This is the amount the employer must remit to the SSS, posted on the employee’s SSS account after payment.

Another way to compute the monthly contribution is using the MSC x Contribution Rate formula.

Again, let’s use the MSC of ₱20,000 as an example.

Employee’s share: ₱20,000 x 0.045 (4.5% contribution rate) = ₱900

Employer’s share: ₱20,000 x 0.095 (8.5% contribution rate) = ₱1,900 (plus ₱30 for the EC contribution)

Total contribution: ₱900 + ₱1,930 = ₱2,830

4. Aside from their regular contributions, select SSS members with MSC of over ₱20,000 are now required to pay for a new provident fund called the Workers’ Investment & Savings Program or WISP.

The WISP is a tax-free retirement saving plan4 that will serve as a supplement to your SSS pension benefits.

Note that among members under the Formal Economy, only employees in the private sector with an MSC of over ₱20,000 are qualified for WISP. Therefore, government employees are exempted and won’t have salary deductions for WISP.

As with regular contributions, the employer will shoulder a significant percentage of the employee’s monthly WISP contribution.

For example, a private employee with a maximum MSC of ₱25,000 must remit a total of ₱700 a month for his WISP account – ₱225 from his salary and ₱475 shouldered by his employer.

No need to visit the SSS office to enroll in this new mandatory provident fund. You’ll automatically become a member once your first payment (for both WISP and your regular contributions) is posted beginning January 2021.

2. Self-employed Members

If you’re registered as self-employed, the monthly earnings you declared on your Form E-1 or the latest Form E-4 will be the basis for your MSC and monthly contribution.

SSS defines you as a self-employed member if you’re involved in a trade, business, or occupation wherein you are your boss.

Using the SSS contribution table as above, here are the steps to figure out how much your monthly contribution is.

1. On the leftmost column (“Range of Compensation”), find the range where your declared monthly income falls.

2. Find your corresponding MSC in the rightmost column of the “Monthly Salary Credit” section. For example, if your declared income is in the range of ₱19,750 to ₱20,249.99, your MSC is ₱20,000.

3. Determine your monthly contribution using the formula:

MSC x Contribution Rate = Monthly Contribution Amount

Let’s say your MSC is ₱20,000, and the contribution rate is 14% (premium rate for 2023); here’s how to compute your contribution as a self-employed member:

₱20,000 x 0.14 = ₱2,800

This is not the final computation, though.

Recently, SSS announced that self-employed members can now register for the employees’ compensation (EC) program5 just like their counterparts in the formal economy sector.

However, you will pay your EC contribution yourself since you don’t have an employer to pay it.

Self-employed members with a monthly salary credit (MSC) below ₱15,000 will pay a monthly EC contribution of ₱10, whereas those with an MSC of ₱15,000 and above will pay ₱30.

Using the same example above, if the self-employed member has an MSC of ₱20,000, the total amount of his monthly contribution will be ₱2,830 (₱2,800 plus EC contribution of ₱30).

Just like private employees, self-employed members with an MSC of over ₱20,000 are also required to pay for the new mandatory provident fund called WISP. The difference is that they don’t have an employer, so they must pay the total amount from their pockets.

3. Voluntary and Non-Working Spouse Members

In the case of voluntary members, it’s tricky to determine the SSS contribution because their income is not fixed.

As such, the SSS only requires people paying their first contribution as a voluntary member to choose any MSC from the contribution table, regardless of their last posted MSC (as a former employed/self-employed/OFW member).

Your choice of MSC as a voluntary paying member depends on how much you receive on a certain month. Practically speaking, you can pay only what you can afford per month.

Meanwhile, a non-working spouse’s monthly contribution is based on 50% of his/her working spouse’s MSC.

Use the table above to find your monthly contribution as a non-working spouse. Here’s how:

1. Determine your spouse’s MSC. Find your spouse’s salary bracket in the leftmost column (“Range of Compensation”). For example, if your husband’s income is between ₱19,750 and ₱20,249.99, his MSC is ₱20,000.

2. Divide your spouse’s MSC by half. Then, determine your monthly contribution using the following formula:

1/2 of your spouse’s MSC x Contribution Rate (14% for 2023) = Monthly Contribution Amount

If your husband’s MSC is ₱20,000, half is ₱10,000.

Based on the formula above, your monthly contribution is ₱1,400 (₱10,000 x 0.14).

If 50% of your spouse’s MSC doesn’t correspond to any MSC in the SSS contribution table, base your contribution on the next higher MSC.

For example, if your spouse earns ₱3,500 per month, 50% of his/her MSC (₱3,500) is ₱1,750 (which is below the minimum MSC of ₱4,000). The next higher MSC is ₱4,000. Therefore, your monthly contribution is ₱560 (14% of ₱4,000).

Just like private employees, voluntary and non-working spouse members with an MSC of over ₱20,000 are also required to pay for the new mandatory provident fund called WISP. The difference is that they don’t have an employer, so they must pay the total amount from their pockets.

4. OFW Members

Related: How to Get an Overseas Employment Certificate (OEC) Through BM Online

For 2023, the minimum MSC for OFW members remains at 8,000.

Using the table above, here’s how to compute your SSS contribution as an OFW.

1. Find your salary bracket in the leftmost column (“Range of Compensation”).

2. Find your corresponding MSC in the “Monthly Salary Credit” column. For example, if your income is between ₱19,750 and ₱20,249.99, your MSC is ₱20,000.

3. Find your contribution amount by using this formula:

MSC x Contribution Rate = Monthly Contribution Amount

Let’s say your MSC is ₱20,000, and the contribution rate is 14 (for 2023). Here’s how to compute your full contribution:

₱20,000 x 0.14 = ₱2,800

Just like private employees, self-employed members, and voluntary members, OFWs with an MSC of over ₱20,000 are now also required to pay for the new provident fund called WISP starting January 2021. For more information, please refer to the earlier sections.

5. Household Employers and Kasambahay

For house helpers with a monthly salary below ₱5,000, the Kasambahay Law requires household employers to pay the total monthly contribution.

However, kasambahays who receive ₱5,000 or higher must share in their contribution payment (4.5% of their MSC). In comparison, their employer pays 9.5% of the MSC plus the EC contribution of ₱10 per worker earning below ₱15,000 or ₱30 per worker earning ₱15,000 and above.

Using the SSS contribution table for household employers and kasambahay, here’s how to compute your monthly contribution:

1. On the leftmost column (“Range of Compensation”), find the range where the current monthly income falls and its corresponding MSC on the Monthly Salary Credit column. For example, if the kasambahay‘s monthly salary is ₱6,000 (the 2023 minimum wage in Metro Manila), his/her MSC is ₱6,000

2a. If you’re a household employer: Find your share of contribution on the HR (Household Employer) column corresponding to your kasambahay‘s MSC. Using the example above (MSC of ₱6,000), you must pay ₱570 for the SSS contribution plus ₱10 EC contribution for a total of ₱580.

2b. If you’re a kasambahay: Find your monthly deduction for SSS contribution on the EE column corresponding to your MSC. Taking the example above (MSC of ₱6,000), your employer should deduct ₱270 (₱6,000 x 0.045) from your salary and remit it to the SSS along with your employer’s share.

3. Look for the amount in the rightmost column to know the total monthly contribution. For example, if a kasambahay has an MSC of ₱6,000, the total monthly contribution is ₱850 (₱270 employee’s share + ₱570 employer’s share + ₱10 EC contribution). This is the amount the employer must remit to the SSS, posted on the kasambahay‘s SSS account after payment.

Another way to compute the monthly contribution is using the MSC x Contribution Rate formula.

Again, let’s use the maximum MSC of ₱6,000 as an example.

Employee’s share: ₱6,000 x 0.045 (4.5% contribution rate) = ₱270

Employer’s share: ₱6,000 x 0.095 (9.5% contribution rate) = ₱570 (plus ₱10 for the EC contribution)

Total contribution: ₱270 + ₱570 + ₱10 = ₱850

Tips and Warnings

1. Update your contact details with the SSS

Updating the contact information in your SSS records allows you to receive a PRN every quarter and notifications and reminders from the SSS. This helps you pay your contributions on time, so you can quickly avail of an SSS benefit or loan when needed.

You have three options for updating your contact details: My.SSS portal, SSS mobile app, or over-the-counter at any SSS branch.

Related: How to Change, Correct, or Update Your SSS Membership Data

a. How to update your contact information via My.SSS

- Go to SSS Member Portal. Answer the captcha question and then click Submit. You have three portals to choose from—select Member.

- Log in to your My.SSS account.

- Hover your cursor over the MEMBER INFO on the main menu. Click Update Contact Info.

- Check the box/es corresponding to the contact info you want to be changed/updated (see the screenshot above).

- Click the Next button.

- Review your edited contact info.

- Click the Submit button.

b. How to update your contact information via the SSS mobile app

- Log in to your My.SSS account.

- Tap the My Information icon > Update Information > Contact Details.

- Edit your landline number, mobile number, and/or email address.

- Tap the Submit button.

c. How to update your contact information at an SSS branch

Fill out the Member Data Change Request Form (E-4) with your updated info.

Put a checkmark on the box next to “Updating of Contact Information” and the specific info for updating (Address/Telephone Number/Email Address/Mobile Number).

Submit your accomplished Form E-4 to any SSS branch. Or write down your new contact details when applying for a benefit, loan, or other SSS program.

2. Always check if your records are correct and updated

You may pay your contributions regularly and on time, but it doesn’t guarantee you’ll get your benefits with no hassle.

Members with a discrepancy in their name, date of birth, civil status, gender, or list of dependents/beneficiaries often suffer delays in processing their pensions or benefits. This could have been avoided had they updated their records with SSS the first time they discovered such discrepancy6.

Therefore, you must submit the required forms and documents to change incorrect details in your data while still not availing of any benefits. For example, a discrepancy in your date of birth may cause a significant delay in processing your pension, as age is an important qualifying condition for retirement.

3. Pay your contribution during off-peak periods

Expect to stand in long lines in an SSS branch on weekdays during lunch break, especially on the last day of the month when contribution payments are due.

At non-bank payment centers, queues can get long right after office hours and every 15th and 30th of the month, when people receive their salary and pay bills.

To avoid wasting time in long lines, pay a contribution on an early weekday morning when fewer people transact, and you’re likely to be among the first in line.

4. Choose your payment channel wisely

If you plan to avail of an SSS benefit or loan soon, paying your contribution at an SSS branch is better since it will go directly to the system and be processed faster. Your contribution may get posted within 24 hours. However, be ready to wait up to 3-4 hours in line when you visit the branch during a busy time.

Banks are not faring any better. Lines are perpetually long in major banks like BPI at any time of the day. Try your luck at a smaller bank like Security Bank, where lines are usually short (or none), though you can pay only if you have a bank account.

Lines are shorter at non-bank collecting partners, but posting can take longer. Choose this payment channel if you’re trying to save time and when there’s no immediate need to apply for an SSS benefit or loan.

5. Consider making advance payments

The SSS accepts advance contribution payments from all members (except for regular employers and employees) regardless of the number of months or years.

Suppose you can afford it like when you get a bonus or commission, pay your contribution in advance. This way, you won’t be tempted to spend your money on unnecessary expenses.

Another advantage of making advance payments is that you need only one PRN for the months or years you’ll pay ahead. For example, if you pay one year in advance, you’ll get a PRN and transact only once instead of getting 12 PRNs and transacting 12 times a year.

However, if the SSS contribution rate increases again, your advance payments may result in underpayments. Pay the difference immediately to avoid getting your advance contributions posted to a lower MSC.

6. Always keep your payment receipts

If your paid contribution isn’t posted online, it helps to have your validated receipts ready to show proof of payment to the SSS and correct the error.

7. Join SSS Worker’s Investment and Savings Program (WISP) Plus for additional retirement savings

For as low as ₱500, you can be part of SSS WISP Plus7, a retirement savings and investment scheme open to all SSS members. This provident fund, unlike the mandatory WISP, is voluntary only. This new investment vehicle aims to boost its contributors’ retirement savings through its rates higher than those offered by banks.

WISP Plus will not be another burden you have to commit monthly. It allows you to contribute only when you want to. No money to save for this month? You can save on the other month instead.

There’s no income or SSS membership requirement to join WISP Plus. As long as you have not filed any SSS benefit claim (e.g., disability, retirement), you’re good to go. There’s no membership expiration even if you fail to save for a long time.

Frequently Asked Questions

1. Is paying SSS contribution mandatory?

It depends on your membership type. SSS coverage is mandatory for the employer, employed, self-employed, and OFW members, so they must contribute.

The Social Security Law mandates employers to deduct monthly contributions from their employees’ salaries and remit them along with their share of contribution to the SSS.

However, SSS coverage is optional for voluntary and non-working spouse members. They’re not required to pay the contribution but can do it to qualify for SSS benefits and loans. And even when they fail to pay for several months, they’re still covered and entitled to any benefit as long as they meet the eligibility criteria.

2. Can expats pay SSS contributions?

Yes. But foreign residents in the Philippines need to have an SSS number before they pay a contribution and enjoy the benefits of SSS members.

Expats must submit a passport (or any two of the following: Alien Certificate of Registration, driver’s license, company ID) for their SSS number application.

Once an SSS number is secured, foreign residents can start paying their contribution following the same procedure as Filipino SSS members.

3. I’m an OFW. Can my family member in the Philippines contribute for me?

Yes. You may assign a representative back home to contribute for you.

Make sure to give your PRN and other payment details. Also, regularly monitor your posted contributions to ensure that your contributions are remitted to the SSS. Alternatively, pay your contribution in your host country at any SSS-accredited collecting partner.

4. Should I convert to self-employed/voluntary/OFW/non-working spouse to start paying contributions on my own?

Yes. To update your membership status to voluntary or OFW, you don’t have to go to an SSS branch. Just access your online account through the My.SSS portal and choose “Voluntary’’ or “OFW” as your membership type when generating a PRN.

However, if you contribute as a self-employed member or non-working spouse, you must fill out and submit two (2) copies of the Member Data Change Request Form (Form E-4).

5. Can I change the amount of SSS contribution I’m paying?

Yes, you can easily update your SSS contribution on your own if you’re a Voluntary, Self-employed, OFW, or Non-working spouse member. Changing your SSS contribution only takes a few clicks in your My.SSS or SSS mobile app account. There’s no need to visit the nearest SSS branch or present your proof of income. Read this guide to learn more.

6. My latest payment has not been posted yet. What should I do?

If you’re an employee, ask your HR or employer to check if your latest contribution has been remitted to the SSS.

Contributing your own? Despite the PRN implementation, you must wait, as it may take a while before payments get posted.

If it has not been posted after over a month, contact the PRN Helpline ([email protected]) to inquire about the status of your last payment.

7. How do I correct the wrong amount posted on my account?

Go to the nearest SSS branch to request verification and correction of your contribution records. Bring your UMID card/SSS ID or two valid IDs and your validated evaluation receipt.

8. I’ve stopped my SSS contribution payment. Can I continue paying now?

Yes. You may start paying your contribution again anytime as a voluntary member to continue enjoying SSS benefits. To become a voluntary member, your age should be below 60. You must have a previously posted valid contribution as an employed, self-employed, or OFW member.

9. What happens if I miss a payment deadline? Can I pay for the previous month?

Ideally, you have no unpaid monthly contribution in your SSS account to maintain your active membership status. Once you become an SSS member, you’re covered for life, even if you miss your monthly payments. There’s no penalty for individual members who fail to pay their contribution for a certain period.

However, the SSS doesn’t allow members to make retroactive payments to qualify for a loan or benefit. You can only continue paying for the succeeding months or in advance, but never for the past unpaid months.

To avoid missing your SSS payments, be mindful of the payment deadline. Here are the respective payment deadlines for those who are required to contribute:

Regular Employers: Last day of the month following the applicable month (e.g., the March contribution deadline is April 30).

Household Employers: Last day of the month following the applicable month or calendar quarter—last day of every three calendar months (i.e., March 31, June 30, September 30, and December 31).

Self-Employed, Voluntary, or Non-Working Spouse: Last day of the month following the applicable month or calendar quarter—last day of every three calendar months (i.e., March 31, June 30, September 30, and December 31).

Land-Based OFW Members: SS Contributions for January to September can be paid until December 31 of the applicable year.

Self-Employed Persons in the Informal Economy (e.g., Farmers and Fishermen): Contributions for any of the last twelve applicable months may be paid in the current month (e.g., August 2023 contribution can be paid from August 2022 to July 2023).

10. My employer is not paying my SSS contributions. What should I do?

Employees whose employers fail to remit their contributions on time are still entitled to SSS benefits. However, they won’t get approved for an SSS salary loan.

If you find out your employer is not paying your contributions, ask your HR or employer about it before filing a complaint at SSS. Try discussing any discrepancy you found in your SS contributions. There might be a delay in either remitting or posting the contributions. Make sure that you have your payslips that reflect SS deductions from your salary before talking with your employer, as it serves as proof of any discrepancy.

Once you inform your employer, follow up occasionally to ensure that action is being taken to fix the discrepancy.

If your employer deliberately avoids paying your contributions for long, it violates the Social Security Law. Delinquent employers are fined from ₱5,000 to ₱20,000 or imprisoned for more than six years to 12 years.

Additionally, they must remit all unpaid contributions plus a 3% penalty for each unpaid month.

If the employer deducted the SS contribution from the employee’s salary but failed to remit to the SSS, the penalty will be imprisonment of not more than 20 years.

File a non-remittance complaint at the SSS branch nearest your employer’s office or business location. Bring your payslip, company ID, Employment Contract, and Income Tax Return (ITR) as proof of employment. Then, proceed to the SSS Accounts Management Section so the SSS Accounts Officer can assist you. The Officer will guide you throughout the process of filing a complaint.

11. When should I stop paying the SSS contribution?

You can stop paying contributions after you make a final SSS benefit claim for total disability or retirement.

Although you only need a minimum of 120 monthly contributions to qualify for a retirement pension, it doesn’t mean you should stop paying contributions once you reach this amount. If you do this, you will only get a small monthly pension and will not be qualified to avail of SSS benefits and loans.

You can file for optional retirement when you’re 60 and unemployed. If you’re 65 or older and still working (or not), you’ll qualify for technical retirement and won’t need to pay an SSS contribution.

However, voluntary members may continue contributing in their retirement years. To increase their retirement benefits, voluntary members aged 60 to 65 with at least 120 posted monthly contributions may still pay until age 65.

Voluntary members aged 65 and above with less than 120 posted monthly contributions may continue paying until they reach the 120-monthly contribution requirement to qualify for a monthly pension.

12. Can I withdraw my SSS contribution?

Unlike Pag-IBIG contributions that can be withdrawn after 20 years, paid SSS contributions cannot be refunded. You can only file a claim for benefits (sickness, maternity, etc.) or claim your pension upon reaching retirement age.

Likewise, members can’t terminate their SSS membership because they’re covered forever. Even after the member’s death, the SSS will pay a monthly pension or lump-sum amount to the member’s beneficiaries.

13. Who are the primary beneficiaries of an SSS member?

Here are the considered primary beneficiaries:

– Legitimate dependent spouse until the member remarries

– Legitimate, legally adopted (legitimated), and illegitimate children below 21 years old

If the member has no spouse or children, the parents (considered secondary beneficiaries) will be the member’s primary beneficiaries.

Without any beneficiaries mentioned above, the member can designate his/her preferred beneficiaries.

References

- Social Security System (SSS). (2022, September 19). New SSS contribution payment schedule for farmers, fisherfolk, self-employed persons in the informal economy to start soon [Press release]. Retrieved February 2, 2023, from https://www.sss.gov.ph/sss/appmanager/pages.jsp?page=PR2022_049

- Cordero, T. (2022, December 20). SSS says contribution rate hike in 2023 to beef up benefit payments. Retrieved December 31, 2022, from https://www.gmanetwork.com/news/money/companies/854991/sss-says-contribution-rate-hike-in-2023-to-beef-up-benefit-payments/story/

- Republic Act No. 11199: Social Security Act of 2018, https://www.sss.gov.ph/sss/DownloadContent?fileName=20190207-RA-11199-Social-Security-Act-of-2018.pdf § 4 (2018).

- SSS to launch the new mandatory provident fund in January 2021. (2020). Retrieved 28 December 2020, from https://www.cnnphilippines.com/news/2020/12/23/SSS-Workers-Investment-Savings-Program-January-2021.html

- Garcia, A. (2020). Self-employed SSS members may now register to compensation program. Retrieved 28 December 2020, from https://www.gmanetwork.com/news/money/economy/759726/self-employed-sss-members-may-now-register-to-compensation-program/story/?amp

- Ignacio, A. (2019). How to maximize SSS membership | Aurora C. Ignacio. Retrieved 3 July 2020, from https://businessmirror.com.ph/2019/10/02/how-to-maximize-sss-membership/

- Social Security System (SSS). (2022, December 15). SSS launches WISP Plus, the newest retirement savings scheme for members [Press release]. Retrieved February 2, 2023, from https://pia.gov.ph/press-releases/2022/12/15/sss-launches-wisp-plus-the-newest-retirement-savings-scheme-for-members

Venus Zoleta

Venus Zoleta is an experienced writer and editor for over 10 years, covering topics on personal finance, travel, government services, and digital marketing. Her background is in journalism and corporate communications. In her early 20s, she started investing and purchased a home. Now, she advocates financial literacy for Filipinos and shares her knowledge online. When she's not working, Venus bonds with her pet cats and binges on Korean dramas and Pinoy rom-coms.

Copyright Notice

All materials contained on this site are protected by the Republic of the Philippines copyright law and may not be reproduced, distributed, transmitted, displayed, published, or broadcast without the prior written permission of filipiknow.net or in the case of third party materials, the owner of that content. You may not alter or remove any trademark, copyright, or other notice from copies of the content. Be warned that we have already reported and helped terminate several websites and YouTube channels for blatantly stealing our content. If you wish to use filipiknow.net content for commercial purposes, such as for content syndication, etc., please contact us at legal(at)filipiknow(dot)net